- Гідрологія і Гідрометрія

- Господарське право

- Економіка будівництва

- Економіка природокористування

- Економічна теорія

- Земельне право

- Історія України

- Кримінально виконавче право

- Медична радіологія

- Методи аналізу

- Міжнародне приватне право

- Міжнародний маркетинг

- Основи екології

- Предмет Політологія

- Соціальне страхування

- Технічні засоби організації дорожнього руху

- Товарознавство продовольчих товарів

Тлумачний словник

Авто

Автоматизація

Архітектура

Астрономія

Аудит

Біологія

Будівництво

Бухгалтерія

Винахідництво

Виробництво

Військова справа

Генетика

Географія

Геологія

Господарство

Держава

Дім

Екологія

Економетрика

Економіка

Електроніка

Журналістика та ЗМІ

Зв'язок

Іноземні мови

Інформатика

Історія

Комп'ютери

Креслення

Кулінарія

Культура

Лексикологія

Література

Логіка

Маркетинг

Математика

Машинобудування

Медицина

Менеджмент

Метали і Зварювання

Механіка

Мистецтво

Музика

Населення

Освіта

Охорона безпеки життя

Охорона Праці

Педагогіка

Політика

Право

Програмування

Промисловість

Психологія

Радіо

Регилия

Соціологія

Спорт

Стандартизація

Технології

Торгівля

Туризм

Фізика

Фізіологія

Філософія

Фінанси

Хімія

Юриспунденкция

What is a budget?

Case 11.1. «Budgeting and strategy»

A budget is a financial plan that sets out, using figures, an organisation's expected future results. For planning purposes, organisations can use many different types of budgets. For example:

- Income and expenditure budgets. These show how much an organisation expects to receive and to spend in future periods.

- Production budgets. These set out how much an organisation must produce in coming periods of time in order to meet demand.

- Profit budgets. These bring together planned sales, costs, and profit figures.

- By creating budgets, managers can:

1. set out a clear plan, involving target figures for defined periods of time

2. communicate their targets clearly

3. motivate employees to achieve these targets

4. control performance by monitoring actual outcomes against planned targets

5. meet the organisation's objectives.

This case study illustrates how Kraft Foods uses budgets to enable it to meet business objectives related to financial performance with a view to achieving its vision: to become 'the undisputed global food leader.'

Kraft has several important objectives related to its vision. These include:

- being the employer of choice

- being a food industry high performer

- becoming an indispensable partner to customers

- being a responsible organisation and a positive force in the communities in which Kraft employees live, work and make its products remain focused and innovative.

Budgets help Kraft to meet these objectives in a planned forward-thinking way.

Budgets are created through consultation with all areas of the business, to achieve a shared understanding about objectives for the future visions of their teams. The Finance team supports and contributes to the work generated by other business functions to build and secure their support for the budget.

To be effective Kraft recognises that a budget must be challenging but also realistic, so that people feel it can be achieved and is worth working towards. One important element is to identify cost savings that can be re-invested to continue to grow Kraft's powerbrands and to develop its people. Reducing costs by eliminating waste is vital in the modern food industry which is driven by price competition and consolidation in the retail sector.

Kraft´s income and expenses budget

A typical budget:

- relates to a defined time period (usually twelve months)

- is designed and approved well in advance of the period to which it relates

- shows expected income and expenditure - income is the amount of money a business receives from its sales.

- includes all capital expenses likely to be incurred in furthering the organisation's objectives - expenses are the costs incurred in order to make those sales.

To help control expenditure the Finance team collates the costs of the business in relevant groups called cost centres, so that analysis can be meaningful and also well controlled by those directly responsible for authorising the spend.

Many companies, including Kraft, use cost centres that relate to particular factories or production units. Within Kraft each manager is assigned clear responsibility for governing the costs which are allocated to his/her cost centre.

The budgeting process enables Kraft to make clear plans for individual cost centres, which build the budget for the whole organisation. The whole purpose of this exercise is to quantify the likely future costs of the whole operation, whilst always maintaining focus on the future plans for the company.

Kraft sells its wide portfolio of products to a variety of different customers; ranging from the corner shop, to the cash and carry and large multinational supermarket chains. In doing so, it incurs:

- raw material costs and production costs to manufacture the products to sell

- marketing expenses associated with any promotional activity including media advertising

- selling expenses involved in selling its goods into supermarkets and other customers

-  distribution expenses when transporting the products from its European and UK factories to the customer.

distribution expenses when transporting the products from its European and UK factories to the customer.

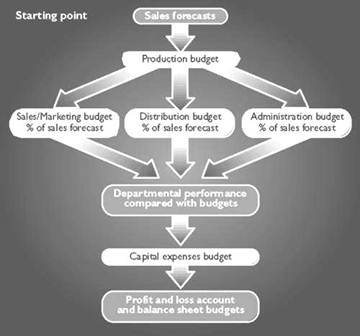

The starting point for building a budget is to forecast the likely sales based on historical information in conjunction with Kraft's and third party understanding of the business environment. This indicates what quantities of products need to be produced and the timing of manufacture.

With these figures in place, budgets can then be allocated for costs relating to sales, marketing and administration, and figures established for the likely costs of storing and transporting the goods (i.e. distribution). These details provide data for relevant departments (e.g. sales, administration etc). Figures can then be inserted for likely capital expenses. The final stage is to construct a budgeted profit and loss account and balance sheet.

Once the budget has been set and agreed by the management teams within Kraft, it becomes the mechanism through which managers monitor progress on a particular business component (for example, a brand, or factory) or on total company performance.

| <== попередня сторінка | | | наступна сторінка ==> |

| Litene social care center for people with mental disabilities | | | The importance of feedback |

|

Не знайшли потрібну інформацію? Скористайтесь пошуком google: |

© studopedia.com.ua При використанні або копіюванні матеріалів пряме посилання на сайт обов'язкове. |