- Гідрологія і Гідрометрія

- Господарське право

- Економіка будівництва

- Економіка природокористування

- Економічна теорія

- Земельне право

- Історія України

- Кримінально виконавче право

- Медична радіологія

- Методи аналізу

- Міжнародне приватне право

- Міжнародний маркетинг

- Основи екології

- Предмет Політологія

- Соціальне страхування

- Технічні засоби організації дорожнього руху

- Товарознавство продовольчих товарів

Тлумачний словник

Авто

Автоматизація

Архітектура

Астрономія

Аудит

Біологія

Будівництво

Бухгалтерія

Винахідництво

Виробництво

Військова справа

Генетика

Географія

Геологія

Господарство

Держава

Дім

Екологія

Економетрика

Економіка

Електроніка

Журналістика та ЗМІ

Зв'язок

Іноземні мови

Інформатика

Історія

Комп'ютери

Креслення

Кулінарія

Культура

Лексикологія

Література

Логіка

Маркетинг

Математика

Машинобудування

Медицина

Менеджмент

Метали і Зварювання

Механіка

Мистецтво

Музика

Населення

Освіта

Охорона безпеки життя

Охорона Праці

Педагогіка

Політика

Право

Програмування

Промисловість

Психологія

Радіо

Регилия

Соціологія

Спорт

Стандартизація

Технології

Торгівля

Туризм

Фізика

Фізіологія

Філософія

Фінанси

Хімія

Юриспунденкция

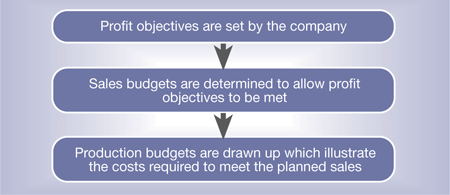

What is a budget?

An organisation must earn enough revenue so that after all costs have been subtracted, there is a profit remaining. One of the most useful financial tools is the budget. A budget is a business plan expressed in financial terms. Budgets can be drawn up for sales, costs or investment spending. A budget will include a degree of prediction of performance which is usually based on past data, e.g. sales.

It is important that it is a realistic financial plan that the business can fulfil. Managers at all levels will have their own budget plans, designed to co-ordinate with and contribute to the overall plan or master budget. Therefore, managers need to be involved in contributing information to the budget to which they will be committed.

Budgets should be stretching but achievable. They should enable companies to meet both short and long-term financial and strategic objectives, whilst providing motivational targets (potentially linked to bonus payments) for managers to promote the right behaviours. All budgets must be carefully monitored, reviewed and, if appropriate, re-assessed as internal factors (e.g. a major project costs significantly less or more than expected) and external factors (e.g. regulatory developments) change.

Budgets should be stretching but achievable. They should enable companies to meet both short and long-term financial and strategic objectives, whilst providing motivational targets (potentially linked to bonus payments) for managers to promote the right behaviours. All budgets must be carefully monitored, reviewed and, if appropriate, re-assessed as internal factors (e.g. a major project costs significantly less or more than expected) and external factors (e.g. regulatory developments) change.

| <== попередня сторінка | | | наступна сторінка ==> |

| Supporting the brand | | | Core business segments |

|

Не знайшли потрібну інформацію? Скористайтесь пошуком google: |

© studopedia.com.ua При використанні або копіюванні матеріалів пряме посилання на сайт обов'язкове. |